Investment in longevity-focused digital health has increased recently. Global longevity-tech startups raised about $9.5 B in 2022, fell to $3.8 B in 2023, then rebounded to $8.49 B in 2024[1]. Deal counts dipped from 385 in 2022 to roughly 325–330 per year in 2023–24[2].

By location, the U.S. dominates this space (home to ~57% of longevity companies and accounting for ~84% of total deal volume[1]), with Europe/UK capturing most of the remainder and Asia-Pacific a smaller share. Early 2025 data suggest U.S. funding is softening while EU funding has stabilized[3], and Asia-Pacific remains active, especially in diagnostics and wearables.

There are five major segments of “digital longevity” (defined below), each with its own trends.

Digital Longevity Five Core Categories

1. Biomarker & Aging Clocks: Quantifying biological age via molecular biomarkers (epigenetic clocks, proteomic profiles, glycan tests).

- Notable Funding Rounds: Tally Health – epigenetic clock app ($10 M seed in 2023[5]); TruDiagnostic, GlycanAge, DeepLongevity, and others (DNA methylation or multi-omic tests).

2. Preventive Health & Lifestyle Optimization: Personalized wellness/coaching platforms using diagnostic data. · Notable Funding Rounds: Function Health – blood biomarker testing & prevention platform ($53 M Series A in 2024[1]); InsideTracker (nutrition & labs, $15 M round[11]); supplement-optimization services (e.g., Thorne, Lifeforce, Superpower Health).

3. Early Detection & Screening: AI-driven or imaging diagnostics to catch disease early. · Notable Funding Rounds: NEKO Health – full-body AI scanning clinics (raised $260 M led by Lightspeed & General Catalyst in 2024[9]); Prenuvo – whole-body MRI screening; Biograph – AI cancer imaging; Healthy.io – smartphone urine tests (raised ~$60 M).

4. Therapeutic Discovery & Geroprotectors: Drug discovery platforms and analytics to find anti-aging therapies. · Notable Funding Rounds: AI/omics drug discovery startups like Insilico Medicine ($110 M Series E in 2025[6]), AgeXtend, Longevity.AI; BioAge Labs ($170 M Series D in 2024[7]); Rubedo Life Sciences ($40 M Series A[7]).

5. At-Home Monitoring & Real-Time Vitals*: Wearables and sensors for continuous health data. · Notable Funding Rounds: Eko Health – AI stethoscope (recent $41 M Series D[8]); ŌURA* – sleep/vital tracking ring ($200 M Series D)[1]; plus wearables like Empatica (seizure detection bracelet), Hexoskin (biometric shirts), CardiacSense (medical watch), CONNEQT Health* (blood-pressure monitor).

*Even though longevity isn’t the core service offering of ŌURA and CONNEQT Health, they offer cardiovascular age tracking and analysis, providing longevity-related advice.

Global Overview: Top Digital Longevity Categories by Funding

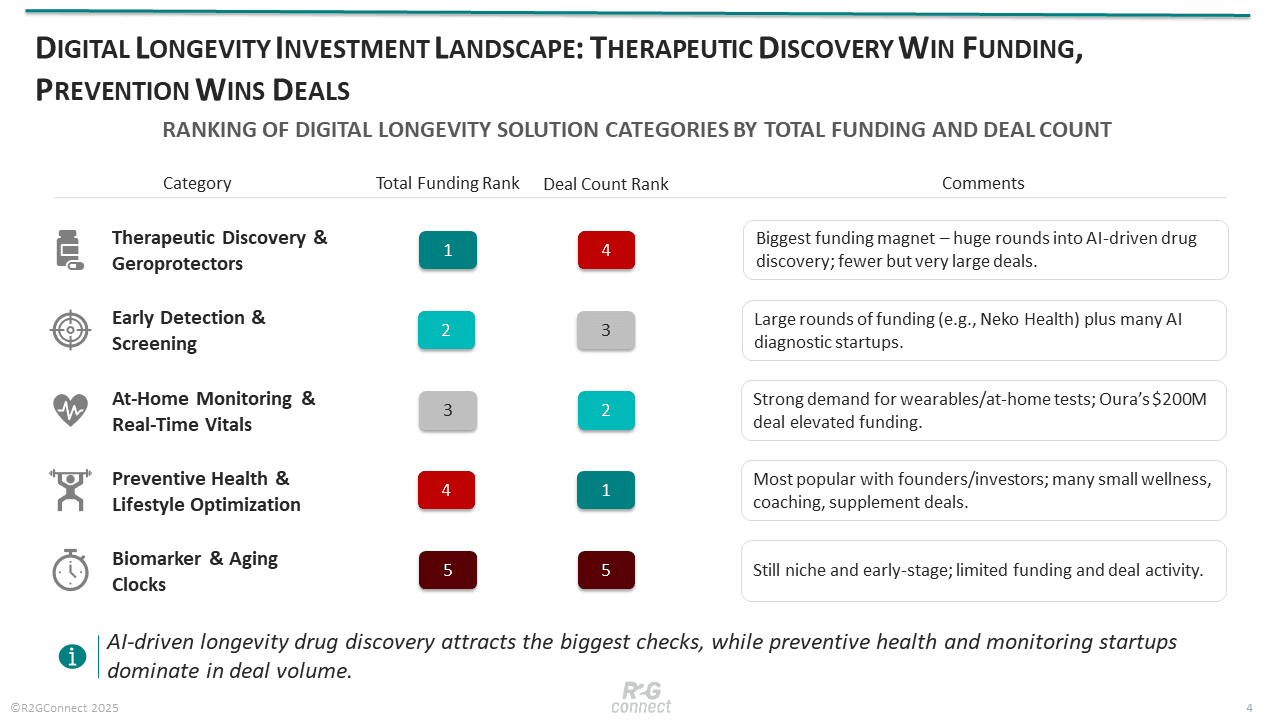

In the past year, Therapeutic Discovery & Geroprotectors emerged as the top-funded category in digital longevity healthtech. Startups providing AI-driven drug discovery and “geroprotector” platforms attracted the lion’s share of capital – roughly $2.65 billion in 2024 (nearly one-third of all longevity funding)[1]. Investors heavily favored these platform technologies supporting therapeutic discovery, reinforcing a strategic industry pivot toward data-rich tools in longevity R&D[1].

By contrast, other digital longevity categories saw much more modest funding levels.

For example, Early Detection & Screening companies (e.g. AI diagnostics and preventive screening services) together garnered around $540 million in 2024, while Preventive Health & Lifestyle startups and At-Home Monitoring solutions each received on the order of only a few hundred million dollars globally[2]. Longevity lifestyle and at-home health monitoring companies (think personalized wellness programs, smart wearables, at-home tests) each raised under $400 million last year[2] – reflecting the earlier-stage nature of these businesses and their lower average deal sizes. The Biomarker & Aging Clocks niche (epigenetic age tests and other aging biomarkers) remains a small but growing segment[2], with many new startups raising seed or Series A rounds; however, total funding in this sub-sector was relatively minor compared to the other categories.

Top Digital Longevity Categories by Deal Count

When it comes to deal volume, the landscape is somewhat inverted.

The Preventive Health & Lifestyle Optimization category likely saw the highest deal count globally in 2024, even though its dollar funding was not the largest. Many early-stage startups worldwide are targeting personalized longevity coaching, supplements, and lifestyle interventions, leading to numerous small venture rounds. In other words, more deals but smaller check sizes characterized this preventive/lifestyle segment[3].

Likewise, the At-Home Monitoring segment (wearables and remote vitals tracking) had countless startups raising seed and growth rounds across the globe, contributing significantly to deal count. Meanwhile, the top-funded Therapeutic Discovery platforms tended to have fewer but much larger deals – a handful of big Series B/C rounds (often $50 M+ each) that drove that category’s funding total[3]. The Early Detection & Screening space sat in between: it saw a few outsized financings (for example, NEKO Health’s recent $260 million Series B[9]) alongside many smaller deals for blood testing and biomarker monitoring startups.

Overall, investors globally poured $8.49 billion into 331 longevity-related deals in 2024[1] – a strong rebound in activity – with digital longevity startups across all five categories attracting funding, but each category playing a different role in terms of investment size versus deal count.

United States: Major Deals and Dominant Categories

The United States is the epicenter of longevity startup investing, accounting for the vast majority of funding and deal activity. In 2024, U.S.-based companies represented roughly 57% of total longevity funding and over 80% of all deals[1]. This dominance means U.S. trends largely mirror the global picture.

Therapeutic Discovery & Geroprotector platforms led U.S. funding by a wide margin, fueled by major VC rounds into AI-driven longevity biotech ventures (e.g. Insilico Medicine’s $110 M Series E)[6]. Later-stage financings for companies like Insilico, BioAge, and others in this category contributed heavily to the U.S. funding total. At the same time, U.S. investors also backed numerous ventures in the Preventive Health and Early Screening arenas. Notably, the U.S. saw significant deals in those areas – for example, a $53 million Series A for personalized prevention startup Function Health[1] – indicating strong interest in consumer-facing longevity solutions.

Overall, the Therapeutic Discovery category claims the highest U.S. funding, whereas Preventive/Lifestyle startups likely account for the highest number of U.S. deals given the many seed-stage investments in wellness, telehealth, and supplement platforms. In short, the U.S. is investing across all five categories, but big-ticket funding is concentrated in AI-driven therapeutics while deal counts are bolstered by a high volume of smaller preventive health and monitoring startups.

Europe: Growing Investment with a Different Focus

Europe’s longevity startup scene is smaller than the U.S.’s but rapidly growing, with some distinct category trends. European companies attracted roughly one-third of the funding of U.S. startups in 2024, and European deals made up only about 10–15% of the global deal count[10]. However, 2024 brought renewed momentum in Europe, and a few standout financings put certain categories in the spotlight.

The At-Home Monitoring & Real-Time Vitals category saw Europe’s largest longevity deal of the past year: Finland-based ŌURA (maker of the Oura smart ring) closed a $200 million Series D to expand its health-tracking wearable, underlining investor appetite for consumer wellness tech[1]. Additionally, in early 2025, Europe scored a major Early Detection & Screening win with Sweden’s NEKO Health raising a $260 million Series B for its AI-powered full-body scanning clinics[9]. These mega-deals helped elevate the funding totals of the monitoring and screening categories in Europe.

That said, Europe’s longevity investments are largely concentrated in earlier stages and preventive “healthy ageing” solutions. European VCs are actively funding Silver Health startups – tools for preventive care, senior wellness, and aging-in-place – but these tend to be relatively small rounds, and there remains a shortage of late-stage funding in this segment[10].

In other words, Europe’s deal flow is boosted by many seed and Series A investments in preventive health and lifestyle optimization, even if each individual deal is modest. Categories like Preventive & Lifestyle and Biomarker/Aging Clock services are well-represented in Europe’s young startup ecosystem, but they did not dominate funding volume. No single category in Europe utterly dominates funding as in the U.S.; however, thanks to the Oura and Neko deals, the Monitoring and Screening segments captured an outsized share of Europe’s 2024–25 funding dollars. Meanwhile, Europe has far fewer big-ticket Therapeutic Discovery platform financings – the largest $50 M+ longevity biotech rounds mostly took place in the U.S. or were led by global investors.

Overall, the U.S. still leads the longevity race in both funding and deal count (American startups raised nearly 3× the amount that European ones did in 2024)[10]. But Europe is picking up speed with a maturing early-stage ecosystem. Notably, the UK has emerged as a key regional hub – it alone attracted more longevity funding than the next four EU countries combined[10] – with a focus on preventive health and lifestyle innovations to help people not just live longer, but live healthier.

In summary, venture funding in 2024–2025 has flowed most generously into AI-driven longevity therapeutics globally, while the greatest number of deals have centered on preventive, lifestyle, and monitoring startups – a pattern exemplified by the U.S. on the funding side and Europe on the deal-count side.

Sources

[1] Longevity investment more than doubled to $8.5bn in 2024. https://www.prnewswire.com/news-releases/longevity-investment-more-than-doubled-to-8-5bn-in-2024--302453871.html [2] 2024 Annual Longevity Investment Report – Longevity.Technology (full-year investment report). https://longevity.technology/investment/report/annual-longevity-investment-report-2024/ [4] HealthTech 250 Thriving Amid Adversity – Mid-2025 Trends & Outlook – Galen Growth report. https://www.galengrowth.com/healthtech-250-thriving-amid-adversity-mid-2025-trends-outlook/ [5] Tally Health Lands $10 M for Personalized Longevity Platform – Fitt Insider (Mar 7, 2023). https://insider.fitt.co/tally-health-launches-personalized-longevity-platform/ [6] Insilico Medicine Secures $110 Million Series E Financing to Advance AI-Driven Drug Discovery Innovation. https://www.prnewswire.com/news-releases/insilico-medicine-secures-110-million-series-e-financing-to-advance-ai-driven-drug-discovery-innovation-302401040.html [7] Longevity Startups Are Getting Funding, But Not As Fast As We’re Aging – Crunchbase News (Oct 2022). https://news.crunchbase.com/health-wellness-biotech/longevity-startup-funding-bioage-alzheon/ [8] Eko Health Raises $41 Million to Scale AI-Driven Heart and Lung Disease Detection. https://www.prnewswire.com/news-releases/eko-health-raises-41-million-to-scale-ai-driven-heart-and-lung-disease-detection-302163975.html [9] Neko Health raises $260 M Series B (press release, Jan 23, 2025). https://www.nekohealth.com/se/en/neko-health-raises-260m-series-b [10] Longevity & Healthy Ageing Report: How Tech is Helping Us Live Longer and Healthier Lives – Speedinvest/Dealroom analysis (Dec 2024). https://www.speedinvest.com/blog/5-takeaways-from-our-longevity-healthy-ageing-2024-report [11] InsideTracker Raises $15 M to Drive Continued Innovation and Delivery of Its Leading AI Platform for Personalized Nutrition and Healthspan Optimization. https://www.prnewswire.com/news-releases/insidetracker-raises-15m-to-drive-continued-innovation-and-delivery-of-its-leading-ai-platform-for-personalized-nutrition-and-healthspan-optimization-301619138.html