The numbers tell the story before the narrative does. Q1 2026 closed at a record $4 billion across digital health, with AI now treated as table stakes rather than a thesis.[1] Mental health led that flow once again — extending the trend from H1 2024, when behavioral health startups captured roughly $682M and topped every other clinical category.[2] But the headline figure conceals a sharper truth: five rounds above $50M absorbed roughly 74% of all mental health capital in 2025–26.[3] Rather than spreading bets, investors are concentrating them on a very specific kind of company.

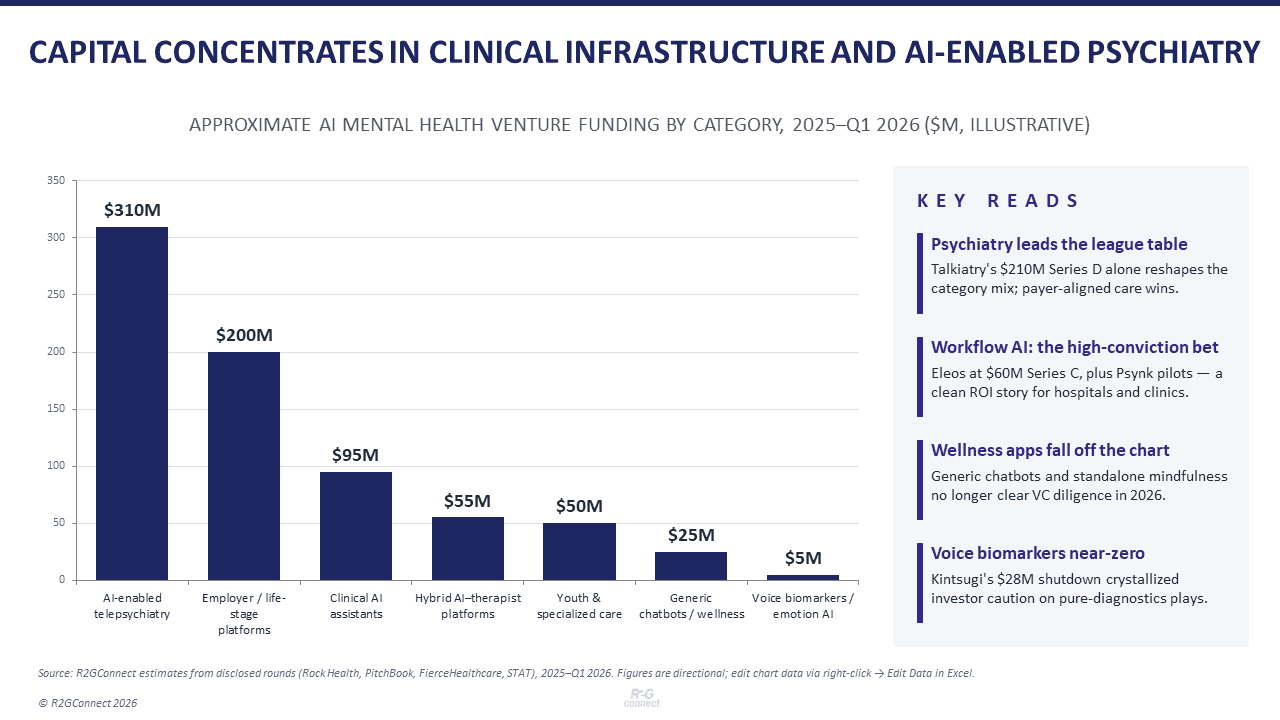

Where capital is flowing 1. Psychiatry copilots and AI-enabled telepsychiatry sit at the top of the stack. Talkiatry's $210M Series D led the Q1 cohort, alongside Blossom Health's $20M raise for an AI copilot embedded in psychiatric workflows.[4] The thesis is straightforward — a chronic psychiatrist shortage, payer reimbursement on the visit side, and AI that extends each clinician's effective panel without asking patients to trust an algorithm with their care. Rock Health captures the pattern as clinical authority paired with payer compatibility.[5] Licensed providers, real codes, software leverage. The cleanest investment shape in the market. 2. Clinical AI assistants — the documentation and workflow layer — are arguably the highest-conviction segment of the year. Eleos Health closed a $60M Series C on the back of 120+ enterprise customers, multimodal models trained on proprietary therapy-session data, and RCT evidence of faster notes and improved patient outcomes.[6] Psynk AI announced pilots inside a psychiatric hospital the same year.[7] Investors like these companies because the ROI is mechanical: less time on notes, fewer compliance errors, more revenue per provider. There is no ambiguity about the buyer or the budget line. 3. Hybrid AI–therapist platforms are the third pillar. Jimini Health raised $17M to embed clinician-supervised AI assistants into therapy workflows, designed from inception to align with CMS and FDA frameworks.[8] Brightside and similar models that pair AI triage with human escalation are getting renewed attention. The pattern is consistent: human in the loop is now a precondition, not a feature. 4. Employer and life-stage platforms remain well-funded but crowded. Spring Health's acquisition of Alma in May 2026 created a mega-platform spanning roughly 170 million covered lives, anchored by Spring's JAMA-published 92% improvement rate among members.[9] Modern Health, Lyra, and Spring are absorbing share. Expect consolidation rather than new entrants here. 5. Youth and specialized care is a quieter but resilient pocket. Handspring Health's $12M Series A, Marble Health's $15.5M, and Affect Therapeutics' $26M Series B point to investor appetite for niche populations where the unmet need is acute and the patient pathway is well-defined.

Where capital allocation is limited 1. Generic LLM chatbots dressed as therapy are the most visible loser of 2026. The APA's caution against using untested chatbots as therapy substitutes has crystallized into VC consensus.[10] Retention is poor, evidence is thin, and the regulatory surface is widening as state-level legislation tightens. Wrappers around public LLMs no longer survive diligence. 2. Standalone meditation and mindfulness apps are commoditized. The Calm-clone segment has saturated, and without a clinical pathway or AI-driven personalization tied to measurable outcomes, the category has effectively been priced out of growth funding. 3. Voice biomarker and emotion-detection startups have shifted from “promising” to “cautionary.” Kintsugi's shutdown in 2026 — after raising roughly $28M for voice-based depression and anxiety screening — became the case study cited in nearly every diligence call.[11] The science is genuinely interesting; the path to FDA clearance, reimbursement, and a workflow buyer is too long for venture timelines. Pure diagnostics plays without a reimbursement hook are now a default “no.” 4. Low-engagement companion bots and journaling tools without clinical integration round out the list. If the product cannot tie into a payer, employer, or provider channel — and cannot produce a measurable health outcome — it is being treated as a feature, not a company.

What the winners share Three traits show up in nearly every funded round. 1. Proprietary data and clinical credibility. Eleos's session corpus and RCT evidence, Spring's JAMA publication, Jimini's regulatory alignment — these are not nice-to-haves; they are the entry ticket. “We don't invest in an app without evidence of efficacy” is now an explicit VC line.[12] 2. B2B or B2B2C economics. The winners sell to clinics, hospitals, employers, or insurers. Recurring contracts embedded in clinical workflow beat consumer subscription economics every time. Reimbursable workflows — digital therapeutics with CPT codes, prescriber-tied tools — carry the most weight. 3. Defensibility through data, integration, or regulation. EHR locks, payer relationships, and proprietary outcomes data create real moats. Where Kintsugi's regulatory hurdle became fatal, Jimini's regulatory alignment became its moat. The same gate can stop you or protect you, depending on how early you engaged it.

What it means for founders The 2026 reset is not subtle. Capital is flowing to companies that make mental health care more efficient, more evidence-based, and more accessible inside existing payment systems. It is flowing away from consumer apps that confuse engagement with outcomes. Founders should plan validation studies early, engage regulators before they need to, and design for clinician and payer workflows from day one. The era of AI plus mental health equals a Series A is over. The era of AI as embedded clinical infrastructure has begun.

Building clinically validated AI-native mental health solutions?

Apply to R2GConnect’s targeted open call and connect directly with healthcare providers, payers, employers, investors, and behavioral health organizations actively seeking next-generation AI mental health platforms for real-world deployment, partnerships, and pilots. Apply here: https://www.r2gconnect.com/briefing-details?recordId=recj4oyFBpyYzkhtr&type=brief

Sources 1. Rock Health, Q1 2026 Digital Health Funding Report — record $4B quarter; AI now treated as table stakes. 2. Rock Health, H1 2024 Digital Health Funding Report — mental health led at ~$682M. 3. PitchBook / CB Insights analysis of mental health funding, 2025–26 — five rounds >$50M ≈ 74% of category capital. 4. Q1 2026 megadeal coverage (FierceHealthcare, STAT, MedCity News): Talkiatry $210M Series D; Blossom Health $20M raise. 5. Rock Health analysis: psychiatry combines “clinical authority with payer compatibility,” 2025. 6. Eleos Health Series C announcement, January 2025 — $60M, 120+ customers, multimodal models, RCT outcomes data. 7. Psynk AI launch and psychiatric hospital pilot announcement, 2025. 8. Jimini Health $17M seed round announcement, 2025 — clinician-supervised AI, CMS/FDA-aligned design. 9. Spring Health acquisition of Alma, May 2026; JAMA Network Open study on member outcomes (~92% improvement). 10. American Psychological Association advisory on generic AI chatbots in mental health. 11. Kintsugi shutdown coverage, 2026 — ~$28M raised; cited FDA and business-model hurdles. 12. VC commentary aggregated from HLTH, Venture news and Rock Health, 2025–26.