A new study by Research2Guidance highlights significant differences in how health insurance companies in the US and EU are implementing AI solutions. These differences are evident not only across specific use cases, but also in how private and statutory health plans adopt AI tools, as well as in which application categories they prioritize.

Where adoption actually concentrates

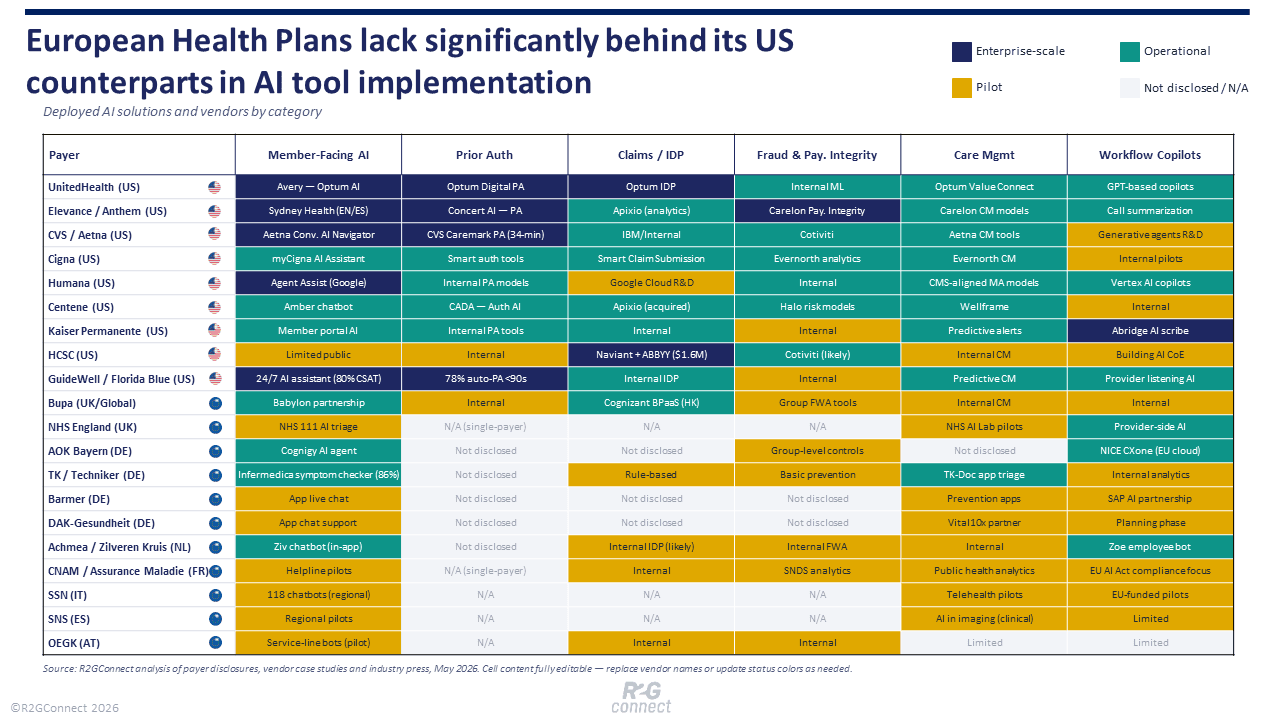

Across the major payers, two solution categories have reached enterprise scale. Contact-center AI — chatbots, voice assistants, and agent-assist copilots — is now operational rather than experimental. UnitedHealth's Avery assistant has rolled out to roughly 20 million members [1]. Humana deployed Google Cloud-powered Agent Assist across more than 20,000 advocates [2]. Florida Blue's 24/7 digital assistant runs at an 80% member satisfaction rate [3].

The second mature category is prior-authorization automation: Florida Blue auto-approves 78% of prior auths in under 90 seconds [3], Optum's "Digital Prior Auth" reports 96% first-pass approval over 500M+ transactions [4], and Elevance/Anthem has cut manual prior-auth work by roughly 70% [5].

Intelligent document processing for claims sits a step behind but is well past pilot — HCSC saves around $1.6M annually on claims automation alone [6]. By contrast, agentic workflow orchestration, generative underwriting, and AI-driven payment integrity at scale remain mostly internal projects with limited public disclosure. The gap between "press-release AI" and operationally embedded AI is widest in fraud, waste and abuse, and in care-management decision support.

The private-versus-public split

Private US insurers and integrated systems behave very differently from European statutory or national payers — even when the underlying technologies are similar.

Private payers like UnitedHealth, Elevance, CVS/Aetna, Cigna and Humana invest in member-facing generative interfaces, branded assistants, and large cloud partnerships. Aetna launched a conversational AI navigator with planned voice enablement [7]. Cigna unveiled an AI-powered myCigna assistant with a built-in governance framework [8]. Integrated provider-payers (Kaiser, GuideWell) push AI deep into the clinical workflow — Kaiser deployed Abridge's ambient AI scribe across its clinicians, with patient consent and physician review as guardrails [9].

Public and statutory payers prioritize data sovereignty, governance, and infrastructure modernization. AOK Bayern moved its 4.5 million-member contact center onto NICE's CXone platform deployed on an EU-sovereign cloud, with Cognigy AI handling intent and call routing [10]. Techniker Krankenkasse integrated Infermedica's AI symptom checker directly into its app, reporting 86% user satisfaction** [11]**. NHS England runs the AI Lab and an oversight framework, but as a single-payer system its AI focus is clinical rather than transactional [12].

The pattern is clear: private US payers race to deploy consumer-grade AI; public European payers modernize the substrate first.

A US-versus-EU read

The geographical contrast is sharpest in generative AI.

US payers have already launched branded generative assistants. European payers, constrained by the EU AI Act, GDPR and statutory governance regimes, more often launch narrower, well-scoped tools: a symptom checker, a routing bot, a sovereign-cloud contact-center upgrade. European payers also rely more heavily on regional vendors (NICE, Cognigy, Infermedica) and sovereign cloud architectures, while US payers integrate directly with the hyperscalers — Humana on Google Cloud Vertex AI [2], CVS and Cigna on OpenAI-class models, UnitedHealth on Microsoft partnerships.

The result: US payers move faster on consumer features, but EU payers often have cleaner data and governance foundations under their narrower deployments.

A look across the top 20

Map the AI footprint of the top US insurers — UnitedHealth, Elevance, CVS/Aetna, Centene, Kaiser, Humana, HCSC, Cigna, GuideWell — and the leading European payers — AOK Bayern, TK, Barmer, DAK, Achmea/Zilveren Kruis, Bupa, NHS England, France's CNAM, Italy's SSN and Spain's SNS — and the dominant solution categories per payer become visible.

- Member-facing AI is near-universal among US private insurers (Avery at UnitedHealth, Sydney at Elevance, Aetna's conversational navigator, Cigna's assistant), with European equivalents typically lighter (TK's Infermedica checker, Zilveren Kruis's Ziv bot, AOK Bayern's Cognigy agent) [13].

- Prior-authorization AI is concentrated in US insurers and integrated systems — UnitedHealth, Elevance, CVS Caremark with a 34-minute median PA time** [14]**, and Florida Blue — and largely absent in the European set.

- Claims and intelligent-document processing is broad but quieter: HCSC plus Naviant/ABBYY** [6], Bupa Hong Kong on a Cognizant BPaaS model [15]**.

- Fraud and payment-integrity AI tends to live under vendor partnerships (Cotiviti, Carelon, EXL Health) [16].

- Agentic workflow orchestration is showing up first inside large US payers but remains pilot-stage everywhere else.

Where the gaps — and the opportunities — sit

Three areas stand out as underbuilt relative to strategic importance.

1. Fraud and payment-integrity AI is operationally critical but publicly under-promoted; very few payers expose the maturity level of their ML models for FWA, leaving room for specialized vendors. 2. Cross-system interoperability AI — moving data cleanly between claims, EHR, social-determinant, and member-engagement systems — is the single biggest blocker that payers themselves cite. 3. And multi-lingual, agentic member engagement is still rare outside a handful of US flagships; European public payers in particular operate in linguistically complex markets but rarely deploy multi-language generative tools.

For startups, the implication is clear: incumbents own member chatbots and claims automation; the open territory is fraud analytics, agentic back-office orchestration, care-management decision support, and interoperability middleware.

For payers, the priority over the next two years is less about deploying another consumer-facing chatbot and more about scaling AI into the operations layer — prior auth, payment integrity, document processing — where the ROI is measurable and the regulatory tailwind (CMS prior-auth reforms, EU AI Act compliance) is real.

The next wave of AI in health plans will not be defined by who launched the most visible assistant. It will be defined by who managed to make AI invisible — embedded in the workflows that decide whether a claim pays, an authorization clears, or a member ever has to call.

=> If you are building a HealthTech solution for health plans, apply on R2GConnect.com now and present your solution in front of decision makers of health plans worldwide.

Open call: Generative AI for Customer Support & Policy Administration https://www.r2gconnect.com/briefing-details?recordId=recfsES7FWZkLKwsi&ref=Art&type=brief

Open call: AI-Driven Claims Management & Fraud Detection https://www.r2gconnect.com/briefing-details?recordId=recb30016gFBtKbeh&ref=Art&type=brief

=> If you are a health plan looking to accelerate the implementation of AI tools, feel free to get in touch with us. We would be happy to discuss further: hello@research2guidance.com

Sources [1] UnitedHealth Group Newsroom — UnitedHealthcare Introduces AI Companion (Avery), March 2026. [2] Humana Newsroom — Humana Redefines the Member Experience with Agent Assist Built with Google Cloud. [3] Becker's Payer Issues — AI in action: How GuideWell is improving the healthcare experience. [4] MarketBeat — UnitedHealth Group Q1 2026 Earnings Report (Optum AI / Digital Prior Auth). [5] Becker's Payer Issues — 5 ways insurers are betting big on AI (Elevance Health). [6] Naviant — Claims Automation Saves One of the Largest U.S. Healthcare Payers $1.6M Annually. [7] CVS Health — Aetna launches leading-edge conversational AI navigation. [8] Cigna Healthcare Newsroom — Cigna Healthcare Unveils Industry-Leading AI-Powered Digital Tools. [9] Kaiser Permanente — Kaiser Permanente Improves Member Experience With AI-Enabled Clinical Technology. [10] NICE — AOK Bayern Transforms Healthcare Service for 4.5 Million Members with NICE's CXone CX AI Platform. [11] Infermedica — Techniker Krankenkasse Case Study. [12] NHS England — Artificial intelligence (AI) and machine learning. [13] Ziptone — Chatbots in customer contact: Zilveren Kruis (Achmea). [14] Fierce Healthcare — How CVS Caremark is using innovative technology to simplify the prior authorization process. [15] PR Newswire — Bupa Hong Kong selects Cognizant for AI-driven BPaaS solution to transform health insurance claims. [16] Elevance Health — How AI Helps Fight Fraud, Waste and Abuse (Carelon Payment Integrity).